Guest Article Series – Cirplus – Part 3

A closer look at the Circular Plastics Economy – Episode #02

Unleashing the dragons of brand owners supply chain power

By Christian Schiller, Co-Founder and CEO at Cirplus

Legendary and probably the best known to the average consumer from the value chain of plastic and recycling. Because we are using their products every day. Yes, I am speaking of the brand owners (aka product manufacturers or original equipment manufacturers (OEMs). In the world of plastics, the heaviest users of plastics come from the packaging industry, followed by construction and automotive. In other words: the three dragons in the Game of Thrones of Circular Plastics — powerful and almost unstoppable once unleashed.

With packaging capturing almost 40% of Europe’s plastic converters demand alone, it is now time for the Coca Colas, Nestlés and Henkels of this world to enter the stage of circular plastics. They are the brand owners of fast moving consumer goods (FMCGs) who need packaging to sell their products across the globe.

Real plastic polluters or real problem solvers — what will it be?

These players in the value chain are starting to feel the most heat from the consumers and regulators alike. Why? With billions in marketing dollars spent to increase brand and product awareness, brand owners are very sensitive regarding their image. Not so great then if the plastic waste pulled out of the stomach of a whale perished on the shores of Australia clearly reads “Procter & Gamble”. Or a once pristine beach is flooded with Coca Cola and PepsiCo bottles.

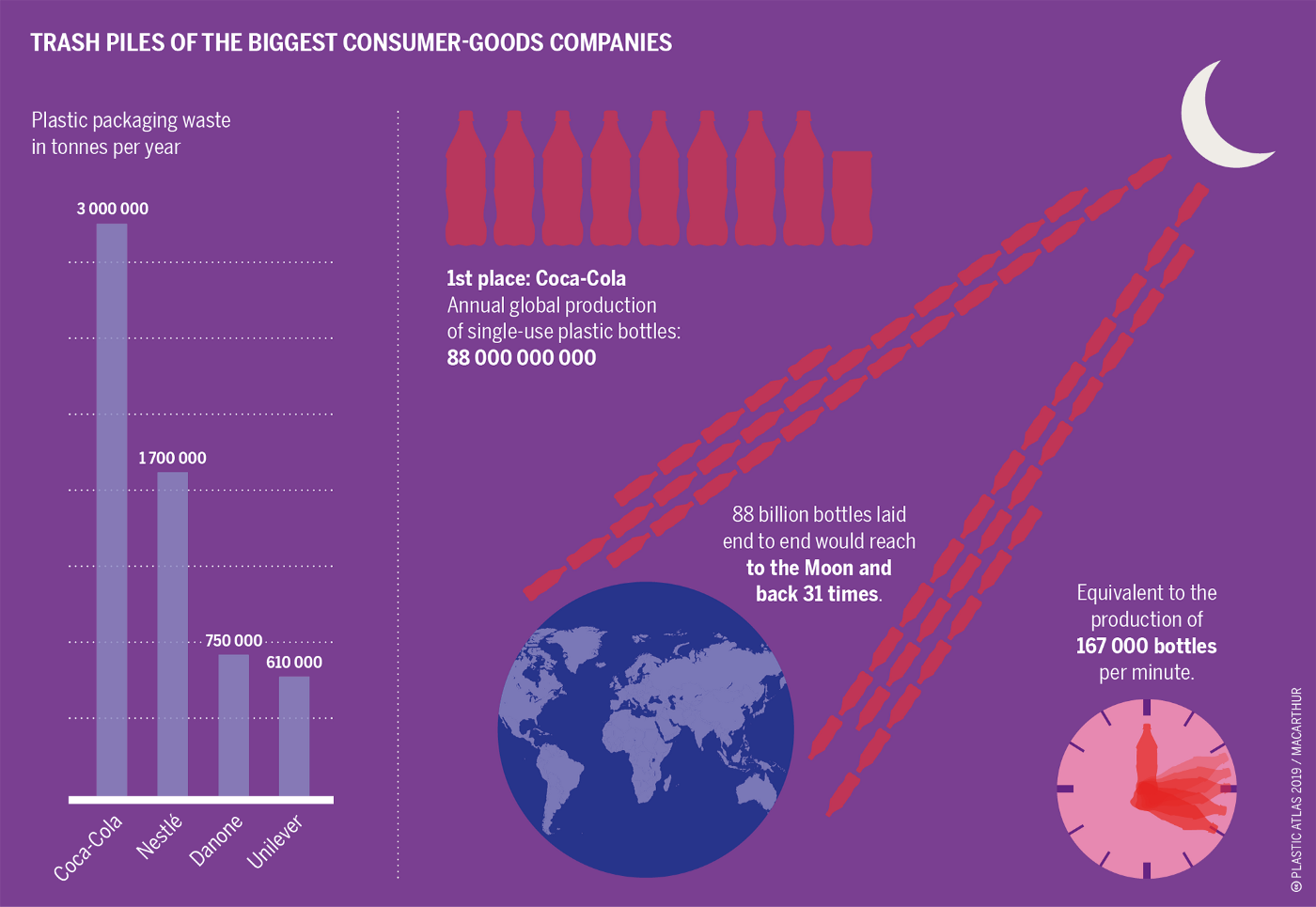

Graphic: PLASTIC ATLAS (2019) | Appenzeller/ Hecher/ Sack, CC BY 4.0

Even before the advent of Fridays for Future, if the brand owners just listened closely to their customers, it would have made them hear an inconvenient truth: “we, the consumers, want change towards more sustainable product manufacturing. We don’t want to buy your packaging, we only need your product. Why use so much plastic? Why make it so hard to recycle? Why are you not using more recycled plastics?”

When called upon by the people, true Targaryens always answer. They are, by all means, self-proclaimed rulers that have the interest of the people close at heart. So they must answer the people’s call. How do they go about that? As diverse as the family of brand owners is, so is their response.

From shifting responsibility to distraction to real efforts — the panoply of brand owners responses

No one in the industry is denying the fact that the plastic consumption that comes with the selling of their products is causing a problem of global proportion that threatens their bottom line. Yet the responses to this ultimate challenge vary widely. From detractors to active change makers. Let’s look at it more closely.

First response: shifting responsibility

One key argument of the industry runs along the veins of: “It is not us who are responsible for all the plastic waste entering the oceans. The real cause are littering consumers and the insufficient waste stream management of the main polluting countries. Why should we be held responsible if the country where we are selling our products did not invest into a proper waste scheme?” An argument that seems plausible at first glance: brand owners are good at producing & selling products, they are not experts in waste management of products that reach the end of their life cycle.

The unpleasant question to ask then: why aren’t they held accountable? Why do so many societies turn a blind eye on the waste that is inextricably linked to the sale of so many FMCGs across the globe? After all, great companies often reject government interventions into their operations, arguing that they know their markets and customers best.

It then strikes me as paradox that with the economic freedom to operate almost anywhere in the world does not come the strong entrepreneurial feeling of responsibility for their products until the very end of their lifecycle (and that includes the necessary byproducts of every product sale, here: packaging). The idea that one is not also responsible for all product externalities, including its treatment at the end of its life-cycle, runs strongly against the notion of an Ehrbarer Kaufmann (a Hanseatic term for honorable businessman). It runs against the very notion of sustainable entrepreneurship.

To be fair, most brand owners acknowledge their responsibility in this or at least seek to assume it. In the packaging industry of many developed nations, they have even been forced to accept it via so-called Extended Producer Responsibility (EPR) schemes, often better known as Green Dot systems. The idea: The EPR companies/institutions collect a fee from every brand owner based on the amount of packaging they use for selling their products. The EPR schemes then organise the end-of-life treatment of the plastic waste, i.e. collection, sorting and treatment (i.e. landfill, export, incineration or recycling). This system works well for countries like Germany, where processing rates of plastic waste nearly reach 99%.

But what do you do in countries where such organised collection and processing does not exist? Here then, many brand owners point at the government’s responsibility to institute such systems. And they have a point: even if you are CocaCola or Nestlé, it does not make any sense to organise the pick-up and processing of the packaging waste your products have caused by yourself, i.e. finance some sort of “CocoCola Waste Collection and Processing Company” that sends out its own trucks. No consumer wants to keep thousands of separate waste bins, one for each brand owner’s products.

Where governments are unable or unwilling to do so, most FMCG producers still sell their products, even though that causes a massive burden on those countries with non-existing waste management systems. And even worse, many of the poorest countries have even accepted to take in millions of tons of plastic waste as an easy way to generate money. Too often, such waste is being accepted and then dumped in nature, burnt uncontrollably or mismanaged in other ways. Very little, if any, of the exported waste is actually being recycled and brought back into the economy. Instead, the ocean is being misused as a dumpsite.

There is no denying it: the main responsibility for all this waste rests with the brand owners. If they would not sell, there would not be any waste. But it is equally true that the consumers would be worse off if such products were no longer sold: after all, they want or even need to consume food, cosmetics, detergents etc. So not selling is not a real option in today’s globalized world. On the other hand, continuing to sell worldwide causes massive environmental leakage, as described earlier.

The second response then is that of improving waste management (i.e. collection, sorting and processing) in countries where such infrastructure is missing.

Second response: Improving waste management

Improving waste collection in those countries where plastic waste is poorly managed, mainly in Asia, Latin America and Africa, is thus the focus of many industry efforts (such as Project STOP or the Alliance to End Plastic Waste). The silent message behind these efforts is: we, the oil-giants, petrochemicals and brand owners, are not really the problem. It’s the poor waste management in the global south that is causing the plastic crisis — a message that almost everybody within the industry can agree with. Because, conveniently, that offloads the problem to poorer nations. At the same time it suggests that, ‘if only we collected the waste better at the end of the product’s lifecycle, the problem of plastic pollution is no more. And we can continue doing business as usual’. (The tagline of Project STOP literally reads: Frontline action to stop marine plastic pollution — not: Frontline action to keep plastic in the loop for as long as we can.)

See the problem? While it is undeniably true that many developing nations have not set up appropriate waste management and recycling systems, even if they would collect 99% of all waste properly, the next dragon in our series enters the room: what do you do with all that collected waste if no one wants to have it? The answers today are the same as always: burn it, export it, landfill it (illegally or legally). But recycling? Nah, that’s not what interests us brand owners all that much.

A mere increase in collection rates of plastic waste will not stop the plastic crisis. ‘Waste always finds the cheapest way’ is a quote I am often confronted with when speaking with waste managers. And all cheap ways lead to environmental leakage and marine pollution. So, in short: it is important to improve waste management in poorer nations, yes. But this is only the very first step. The tougher step is to reinsert such collected waste into a second, third, fourth life cycle, ideally as the same product it was before (this is what is called “closed-loop-recycling” or “bottle-to-bottle”-recycling). And this is where the real challenges in the circular plastic economy begin.

Third response: the real efforts — between pledges and progress

At the high end of the spectrum, real efforts are beginning to be undertaken by brand owners to integrate recycled plastic into their products. The reasoning behind that: if we, the brand owners, create demand for recycled plastics, then businesses and entire economies have an interest in turning plastic waste feedstock into recycled plastic, rather than burning or dumping it. Thereby, triggered by the brand owners demand for recycled plastics, we are creating an economic opportunity out of what was previously just seen as an economic burden. Turning waste into real revenue. Sounds like a far away dream of sustainability nerds? Buckle up and get ready for some really inspiring news.

A recent feasibility study undertaken by packaging experts at Henkel AG, a large German brand owner, offers real prospects for the future of circular plastics. The study takes into account Corporate Social Responsibility (CSR) efforts, bottom line calculations and consumer acceptance in the future of packaging of FMCGs. The study looks at the packager for a brand owners product line with an annual demand for plastic of 10.000 tons of HDPE (High Density Polyethylen) and 10.000 tons of PET (Polyethylenterephthalat) — two of the most commonly used types of standard plastics in packaging.

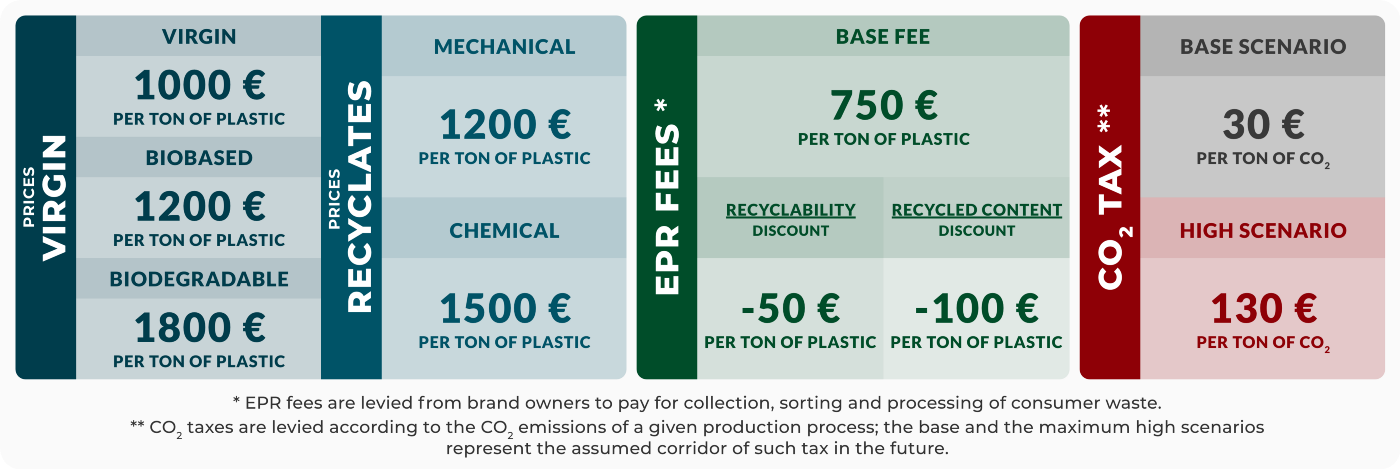

Prices and fees for procuring plastic and bringing it to market in 2030. Translated from Th. Müller-Kirschbaum, Th. Leopold (2019), Are we choking in plastic waste? Scenarios for sustainable and circular use of plastics; in: J. Gausemeier (ed.): ‘Vorausschau und Technologieplanung, 15. Symposium für Vorausschau und Technologieplanung, (Vol. 390, pp. 427–451), Paderborn, Heinz Nixdorf Institut.

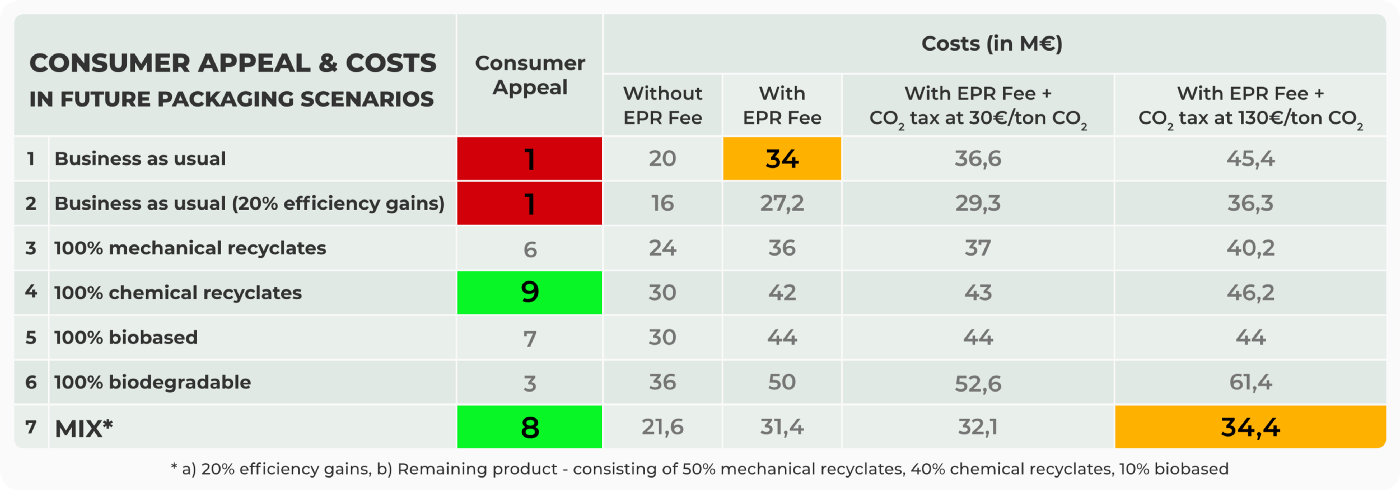

Consumer appeal and costs in future packaging scenarios. Translated from Th. Müller-Kirschbaum, Th. Leopold (2019), Are we choking in plastic waste? Scenarios for sustainable and circular use of plastics; in: J. Gausemeier (ed.): ‘Vorausschau und Technologieplanung, 15. Symposium für Vorausschau und Technologieplanung, (Vol. 390, pp. 427–451), Paderborn, Heinz Nixdorf Institut.

A lot of numbers and assumptions to digest, so it is worthwhile to dig into the entire study, given that it offers a glimpse into the strategic reasoning of one of the largest FMCGs producers in the world. The first graphic states the costs of procuring plastic and the associated fees that come with selling it as packaging (including the EPR fee, see above for reference). The second one lists seven technology scenarios for the future of packaging and pits their respective consumer appeal against the associated costs.

Crucial take-aways for the year 2030:

a) consumers will no longer accept unsustainable packaging made purely from virgin packaging (consumer acceptance = 1, the lowest score possible);

b) consumers would favor chemically recycled plastics (consumer acceptance = 9, highest acceptance, assuming it would “look and feel” like virgin plastic, but marketed as “sustainable plastic”), but it would lead to prohibitively high costs in a world with CO2 taxation.

c) taking into account both consumer appeal and economic viability, the most attractive scenario is that of a packaging mix that uses 20% less material and consists of 90% recyclates and 10% bio-based virgin plastic. Even in the most expensive scenario where the CO2 tax is as high as 130€/ton of CO2 and an EPR fee is applied, such a packaging would cost about €34.4M. This is roughly the same amount it would cost a brand owner and their packager to do business as usual, if no CO2 tax whatsoever is applied (€34M). When applying the same CO2 tax, the packaging mix scenario even becomes significantly cheaper (€34.4M vs. €45.4M — see in figure above).

So the most important takeaway is this: even in a world where at first glance recycled plastic remains more expensive than virgin plastic at procurement level, it makes more business sense for a brand owner and its packager to build a sustainable form of packaging. That’s the message the world of circular plastics needs: brand owners that are willing to accept a higher procurement price for recycled plastic, which ultimately is still better for its bottom line and sustainability targets.

The key to solving the plastic crisis: It must make overall more business sense for brand owners to purchase recycled plastic over virgin content.

Today, in the world of 2020, this scenario does not yet reflect reality, even though we see promising signs from a combination of regulatory and consumer pressures. However, this study should inspire entrepreneurs, regulators, investors and innovators alike to see a glimpse of the future — and to prepare for it accordingly.

Voluntary pledges in anticipation of more regulatory pressure

While we just looked at a silver lining for sustainable plastics, there is still a long road ahead. And brand owners warily look towards regulators when and where the next set of more stringent sustainability regulation will strike, forcing them to adapt their supply chain and production processes sooner than they would like.

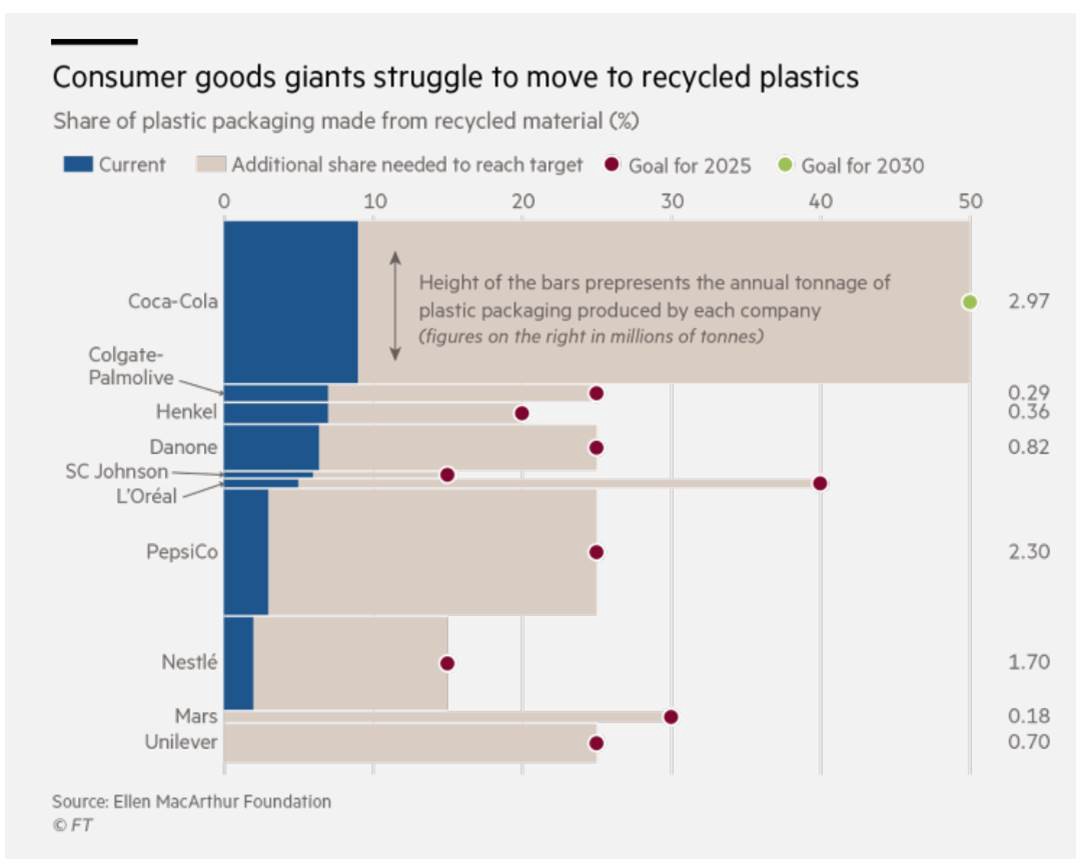

In anticipation of such additional regulatory burdens being put on their shoulders, we can witness a remarkable development: extremely ambitious voluntary pledges by the brand owners to meet high levels of recycled content and recyclability of their products by 2025 and 2030. The most prominent being that of Nestlé announcing earlier this year that it would invest 2 billion Swiss Francs in creating markets for food-grade (!) recycled plastics.

“No plastic should end up in landfill or as litter. Making recycled plastics safe for food is an enormous challenge for our industry. That is why in addition to minimizing plastics use and collecting waste, we want to close the loop and make more plastics infinitely recyclable. We are taking bold steps to create a wider market for food-grade recycled plastics and boost innovation in the packaging industry. We welcome others to join us on this journey.” —Mark Schneider, CEO Nestlé, January 16th, 2020.

Now that’s a statement. That is more than the about 50 companies assembled in the Alliance to End Plastic Waste pledge to spend to organize better waste collection and management in South East Asia and elsewhere. It almost seems like a competition about who can out-do the other for an even more ambitious pledge. Here we see the power when the capitalistic dragon is finally let loose on achieving more sustainable plastic markets: Pledged demand drives investment, spurs innovations and capacity build-up, which in turn will bring down the marginal costs for recycled plastics. Voilá, that is the recipe for redeeming this valuable material while also holding those that benefit from selling their products responsible for the packaging around it.

So then, all is clear it seems? With armies of packaging and procurement experts gathered and with tons of financial resources at their disposal, the brand owners can now set course for Circular Plastic Westeros, i.e. having their plastic ships sail towards a future where plastics will be 100% circular. Consumer demands will shift investments and ultimately turn plastic waste into a thing of the past. They will rightly claim the throne of circular plastic and all will be good in the end…

…well, you guessed it, breaking the vicious plastic pollution cycle is still riddled with a set of enormous challenges for the brand owners. These concern product design (design for recycling) and sales strategy, feedstock security and the question of defining what really is “recycled plastic” (recycled content).

Product Design vs. Marketing vs. Procurement vs. Sustainability

In light of all of the above, imagine the following debate at a large brand owner in the space of FCMGs — we call it the Targaryen Corporation.

CEO (she goes by the name Danaerys): “Okay team, we have to start being serious about keeping plastic in the loop. We have joined the EllenMacArthur Foundation’s Global Commitment, the Circular Plastic Alliance and I just gave a speech in Davos about how we care about our planet. Given our role in the market, I believe we can, and must, drive this process by starting to reduce the use of plastic overall. But even more importantly, we have to make our packaging more recyclable and at the same time increase our use of recycled content (post-consumer plastic that is) to 30% — within the next five years. Sounds crazy, I know, but I believe in this vision. Where do we stand?”

Source: cirplus GmbH

VP Packaging design: “Okay Danaerys, great idea, I am with you. Today, we are using less than 1% recycled plastic across all our packaging, and that 1% is all from post-industrial recyclates. Also, it will be a tough ride because we don’t want our shampoo bottles and other packages to break on the way to the retailer or for our food to perish or even get contaminated due to the recycled plastics.

CEO (shifting uncomfortably in her chair): “Mh, okay, so that’s a 30-fold increase in our use of recycled plastics from post-consumer sources. So maybe we achieve this last or we can use post-industrial recyclates instead for now, since everybody is confused about the clear definitions anyway. What would be the economics of such scenarios?

VP of Procurement: “Danaerys, again, great idea, I am with you. Only, the prices of virgin resins stand at 30% less than that of recycled resins available in the market. And the quantities of high-quality recyclates is very limited. We will have a tough time sourcing enough material at an acceptable price and with acceptable raw material security. Not to speak of our plastic converters, who probably will not be super happy about such a heavy shift in production process.”

CEO (with eyes wide-open): “Really that expensive? Surely the price difference between virgin and recycled will decrease once the Corona pandemic is under control because then oil prices, and in turn virgin price, will rise again. And the recyclers or the petrochemicals better get their act together because we mean business. We need these recyclates. Why aren’t there more recyclates available in the market today?

VP Packaging Design: “Danaerys, as I said, we use less than 1% of recyclates. It just didn’t make sense for us in the past for performance reasons to seriously look into using more recyclates. And with no demand for recyclates in the past, why should there be such significant supply available? Recyclates are just not the same as virgin.”

VP Procurement: “…not to mention the much higher prices for recyclates than virgin resins.”

CEO: “Okay, so I understand we must suffer before things can get better in the space of packaging our products. But surely our customers will reward us for our sustainability efforts. Our sales should go up and we win market shares. The people will love us and our products instead of fearing us and calling us plastic polluters all the time. I see a glorious future for us, even if we have to increase prices a bit for such change and…”

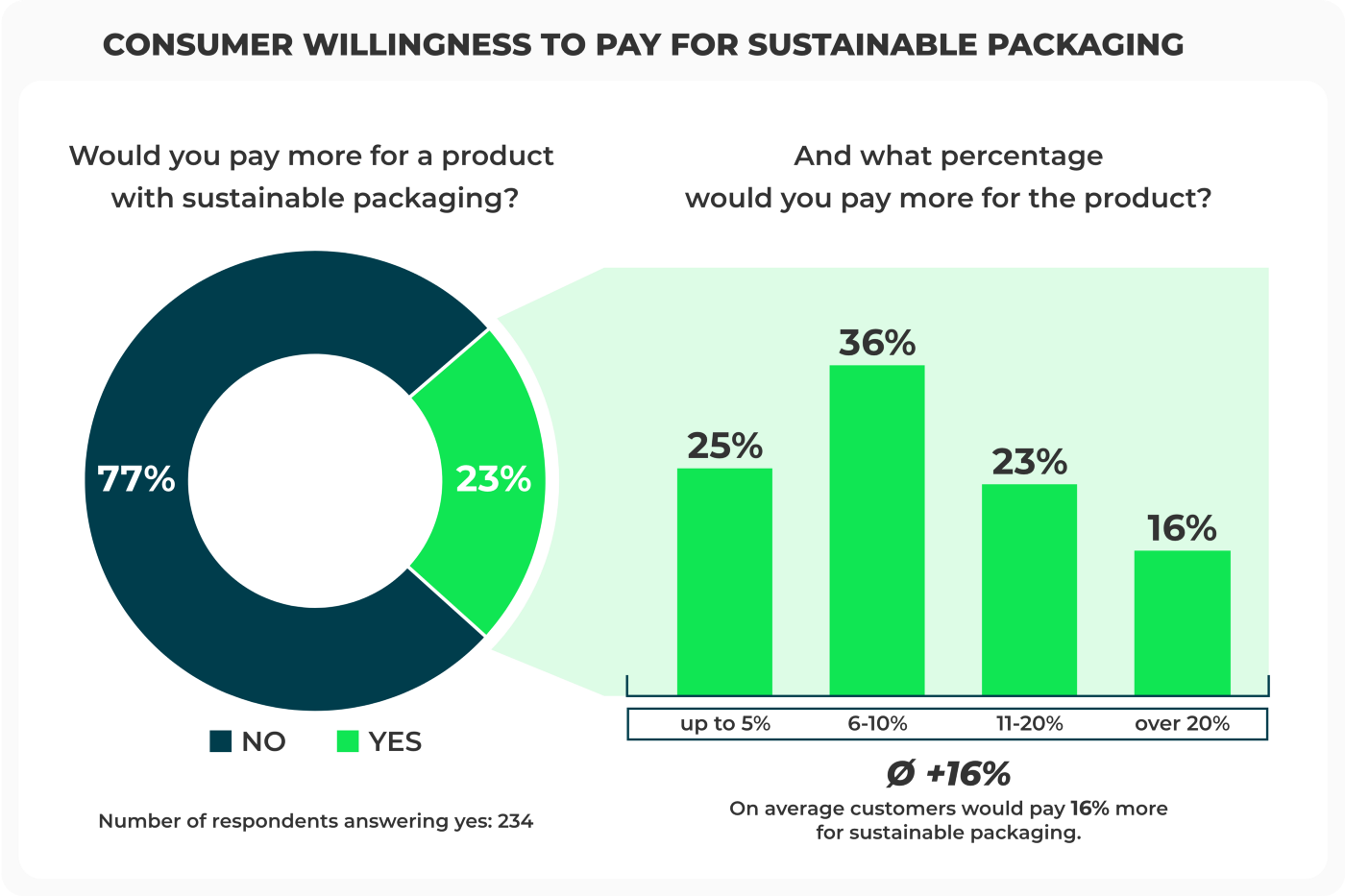

VP Marketing & Sales (clearing her throat): “Ehm…Danaerys, I don’t want to interrupt your enthusiasm there but consumers are very fickle in their convictions. Sure, they scream “less waste, more sustainability” right now. But have you seen the latest consumer study we took among 10.000 consumers in 9 different markets? Yes, they want more sustainability, but they are still very price-sensitive: their willingness to pay a higher price for more sustainably sourced packaging ranges is still very low.

Source: PricewaterhouseCoopers (2018), Verpackungen im Fokus [“Spotlight on packaging”], p. 27. Total Amount of respondents: n=1000.

Not to forget: When we use more recycled plastic and thus accept that our shampoo bottle is not as white as it used to be, we will suffer in our sales. Consumers subconsciously associate such colors with less purity or cleanliness. The sales trough will be quite a long one if we move first. And we would have to start completely rebranding some of our most iconic products, where we spent millions in branding and the marketing of a very specific packaging design. But yes, maybe it’s time for our consumers to accept different designs and truly embrace what sustainability in packaging also means for them…”

CEO (rising level of disengagement from the debate): “So to sum it up, you are saying the plans I announced will cost us a lot of money, will by no means guarantee us a gain in market shares, instead will probably lead to a big decrease in our revenues, and will expose us to a greater instability in our supply chains?….Maybe it wasn’t such a good idea to be so daring?

..but then again, if we miss our voluntary targets, we can say that it wasn’t for lack of trying. I wonder if I will get our sustainability plan through the next board meeting. Maybe I should bring my dragon to make them come in line and follow my vision.”

(All others in the room silently nod with their heads. The meeting is finished as Danaerys storms out of the room, just when the VP of Corporate Social Responsibility was about to present the annual sustainability report).

This meeting probably took place one way or another across the entire world of brand owners. Making plastic packaging more recyclable and increasing the recycled content in packaging, while also not hurting your bottom line and jeopardizing the security of your supply chain, is a really tough nut to crack. The struggles within such corporations will run along various fault lines:

- Procurement: interested in stable supplies at the best price

- Product Design: interested in optimal protection and convenience during the use phase; making products more recyclable often compromises on these parameters.

- Sales & Marketing: interested in protection of the brand image & customer appeal for marketing reasons: Color, smell, the “touch & feel”.

And as an afterthought: It is still unclear how the increased use of recycled plastic in packaging products will affect its recyclability in turn.

There are even more challenges that can be added to the list, but these are arguably the most significant ones. And they are reflected in the boardrooms of brand owners and OEMs in other industries, too. Car manufacturers who are wary of performance issues and consumer appeal impact have rejected the use of recyclates in car parts. However, resistance there is slowly melting in order to bring down the CO2-footprint of their cars. The same applies for other plastic-consuming industries, too.

The good news is: large brand owners have the power to make changes in the supply chain. And once they touch the design of their packaging, they will not just do it for an isolated market.

This opens up great possibilities — and responsibilities — for regulators at national and international level. When change at international level is slow to come about or stalled, even national measures will have an effect on the brand owners. Because they rarely touch their product design simply for one isolated market.

Stay tuned as our series will turn to these regulators next, their efforts, successes and failures.

We have asked cirplus, the Climate-KIC supported recyclates marketplace, to give us an insight into the plastics market from a start-up’s perspective. In the upcoming article series, Christian Schiller, Co-Founder of cirplus, is taking a closer look at the challenges of the circular plastics economy these days. The full series will be published in the following weeks. Join our LinkedIn group to stay tuned!